Quarter four (Oct-Dec) of 2025 (Q4 2025) saw Kiwi shoppers spread their Christmas online purchases over a longer period, resulting in an extended sales period. The result was strong growth that exceeded expectations, with online spending growing 12% compared to Q4 2024. This growth in spending was largely driven by strong transaction growth.

The numbers for Peak 2025 tell a compelling story of adaptation, sending a clear signal that New Zealand's online shopping transformation is accelerating. While instore spending managed a modest 2% increase, online shopping (including offshore and click and collect) dominated the narrative with 14% growth in online transactions, leading the way for total retail spending to rise by 5% compared to Q4 2025.

Key Q4 2025 trends:

- Online share of spending increased by 2 percentage points, cementing digital's growing importance in how Kiwi shoppers buy.

- Transaction volumes drove growth, with shoppers buying online more frequently.

- International transactions grew faster than domestic transactions, but domestic retailers enjoyed higher average purchase values.

- Individual sales event spikes were replaced by a long, extended Peak sales period.

- Growth was experienced across all sectors and regions, but at different rates and in different ways.

- New opportunities are emerging for retailers adapting to the new higher frequency, smaller basket size environment.

The numbers behind the growth

The growth story of Q4 2025 is fundamentally about transactions. Online transactions jumped 14% compared to Q4 2024, more than offsetting a 2% decline in average basket size. This pattern continues to suggest Kiwi shoppers are becoming more strategic, making more frequent purchases online but being selective about what goes in their cart. Shoppers continue to look around for deals, actively substitute products for higher-value alternatives, and to make active decisions about purchase volumes and timing.

Retailer’s response has fuelled the trend by being ‘on sale’ for longer. Some retailers effectively ran ‘Black Friday’ sales for most of the period, while others swapped one promotion for the next. It’s not surprising then that shoppers, started their Christmas shopping earlier, picking up deals as and when they saw (and could afford) them.

Q4 2025 vs Q4 2024 Snapshot

Online spending + 12% | Online transactions + 14% | Online average basket size - 2% |

Instore spending + 2% | Total retail spending + 5% | Online domestic spending % + 0% |

Instore (offline) spending on physical goods in Q4 2025 was up 2% compared to Q4 2024, driven by a modest 1% rise in both instore transactions and instore average basket size. Total retail spending on physical goods, online and offline, was up 5% on Q4 2024, underpinned by growth in transaction volumes and average basket size. Online’s performance was hugely influential in what was a much needed good quarter for retail overall.

The domestic vs international mix

During the quarter, over three-quarters of online spending was with local retailers but that doesn’t tell the full story. While the growth in spending with NZ-based online retailers, as a percentage of total online spend, remained almost flat (0%), the story becomes more nuanced when we examine transactions. International retailers significantly outpaced domestic ones in transaction growth (24% vs 10%), but New Zealand retailers saw their average basket size grow while international baskets declined (-2% vs -11%). This highlights a trend we’ve seen becoming increasingly prevalent in recent years: offshore retailers are winning on frequency and price, while domestic retailers are maintaining value through larger purchase amounts.

HELPFUL HINT FROM NZ POST

Compete on convenience: International retailers are winning on transaction frequency. Combat this by streamlining your ordering process, offering subscription services, automating repeat purchases, revisiting your product mix and creating compelling reasons for customers to return more often. Small, frequent purchases can build stronger customer loyalty than sporadic large orders.

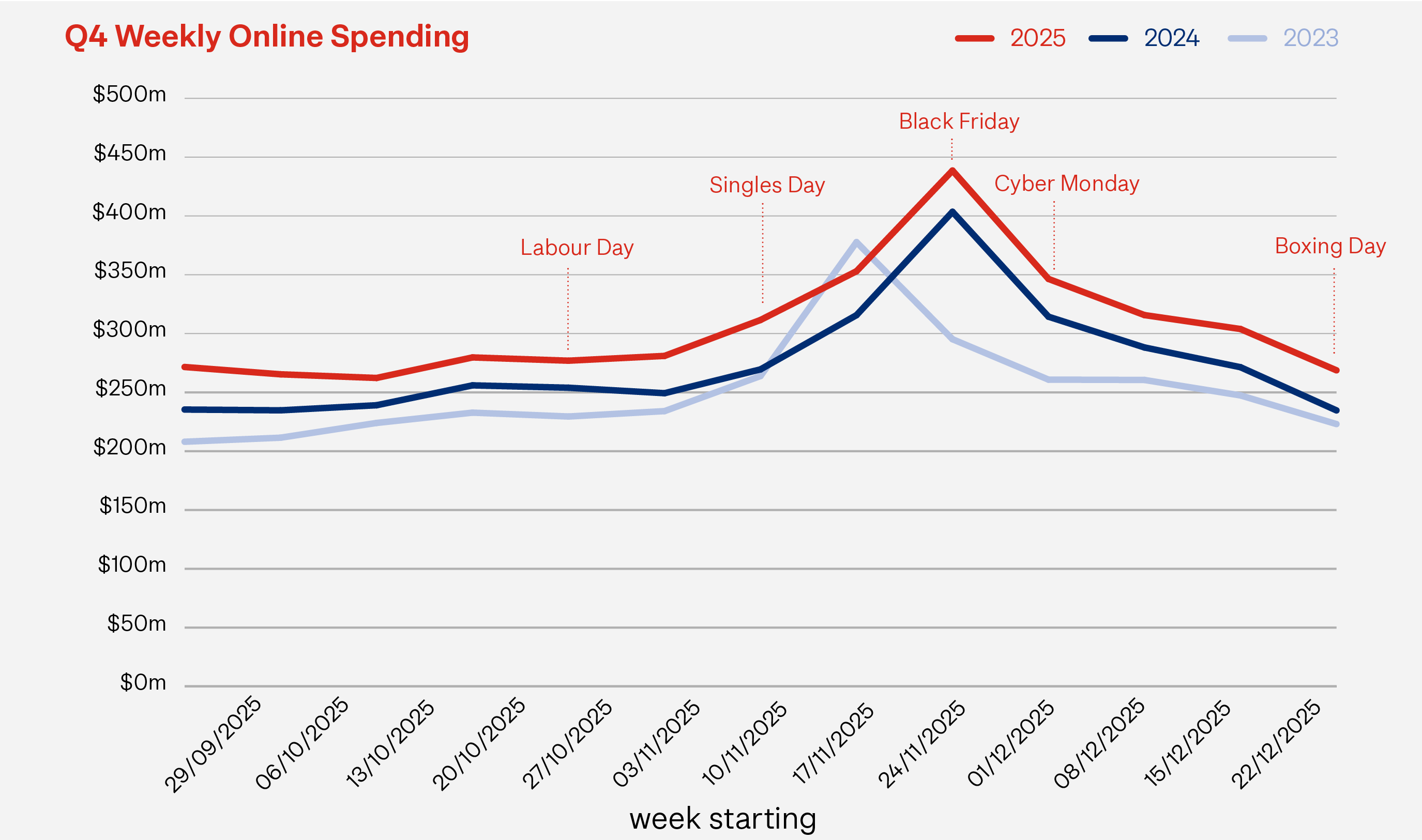

Peak shopping days: An extended sales period

2025 Q4 Peak season looked remarkedly similar to last year, with online spending and transactions rising from Labour Weekend in late October, peaking in the week of Black Friday sales and steadily declining to Christmas. This extended sales period has seen fewer sales spikes than in recent years, with each individual sales event not having the urgency it once had. Shoppers are prioritising convenience and spreading the financial load, over the traditional sales rush. Some retailers caught on to this early, driving sales for earlier events, by promised to refund the difference if they offered a better price at a later point during the period.

Singles' Day success

Singles' Day 2025 delivered significantly higher online transactions (39%) and spending (43%) compared to 2024. Basket size was also up 3%. The day of the week matters, and Tuesday proved far more conducive to online shopping than 2024's Sunday timing, a day when consumers typically show lower online engagement. Instore spending also experienced strong sales growth, up 15%, driven by strong transaction growth and a modest increase in basket size.

Singles’ Day is becoming a more established part of the local retailer’s calendar, catching up to the higher profile it has in international market. Many retailers release their Black Friday offers early to cover Singles’ Day sales.

Black Friday to Cyber Monday: The peak of Peak

Black Friday, Cyber Monday and the week that follows continues to be the quarter’s clear winner. Black Friday to Cyber Monday weekend 2025 saw online transactions up 11% and online spending climb 10% compared to 2024. Average basket sizes dropped 1% from a year ago.

Instore performance showed positive results also, with transactions and spending both up 2% on 2024. The combined online and instore performance (transactions up 3%, spending up 5%, basket size up 1%) reinforced that this period remains retail's most important revenue week. Increasingly, retailers need to segment their Peak promotional plans by pre, during, and post Black Friday to Cyber Monday weekend.

Pre-Christmas: The extended decline

Unlike many previous years, Q4 2025 saw online spending decline steadily after Black Friday through to year-end, without the mini-peaks we often saw in the week before Christmas. This continues a significant shift from traditional shopping patterns and suggests consumers are getting their Christmas shopping done earlier and/or spreading purchases throughout the extended sales period.

Instore spending followed a more traditional pattern, falling immediately after Black Friday before recovering in the week starting December 15 as shoppers rushed to complete their last minute Christmas shopping.

Boxing Day: Reduced importance

Boxing Day 2025 presented a more complex picture. Online transactions grew 3% compared to Boxing Day 2024, but spending dropped 1%, reflecting smaller average basket sizes. Instore spending was also weaker than 2024, with transactions down 1% and spending falling 3%.

The overall result was a Boxing Day that failed to match 2024's performance across all metrics. This is a notable shift for what has traditionally been one of retail's biggest days. After an extended period of sales activity, the last big sale of the year may have seen shoppers experiencing sales fatigue. Retailers, especially those with excess stock left at the end of the sales period, may need to consider how to invigorate shopper enthusiasm in these last few days of the year.

HELPFUL HINT FROM NZ POST

Refine your peak strategy: With individual sales days losing some impact, consider how you can capture value throughout extended sales periods. Focus on customer lifetime value rather than short-term spikes, and use data to identify when your specific customers are most likely to purchase.

Sector spotlight: Winners and opportunities

Q4 2025 showcased impressive growth across most sectors. Several smaller categories delivered standout performances that suggest emerging opportunities for retailers in those sectors to capture their consumers’ growing comfort with buying online. The larger categories also fared well but continue to see international competition intensify.

Largest sector spending increases - Q4 2025 vs Q4 2024

(Share of Q4 2025’s total online spending)

Miscellaneous & + 45%Share: 5% | Health Retail: + 41%Share: 3% | Lifestyle Retail: + 32%Share: 2% |

Furniture & + 23%Share: 8% | Books & Stationery: + 21%Share: 1% | Fashion & Accessories + 19%Share: 3% |

Looking at the 3 largest categories:

Apparel (21% of Q4 2025’s online spending) dominates the online landscape with 11% spending growth, driven by increases in both transactions and basket sizes. The divergent patterns between international and domestic retailers suggests a significant changing behaviours. International retailers seeing greater frequency (16% transaction growth) while domestic players maintain higher-value baskets (2% basket size increase) indicates growing consumer trust in offshore platforms for frequent, lower-risk purchases. Meanwhile, domestic retailers are becoming the destination for purchases where quality, fit and fabric matter most.

Interestingly, this online apparel growth isn’t matched offline, with instore apparel transactions and spending declining compared to Q4 2024. The shift suggests shoppers are now more comfortable than ever buying clothes sight-unseen.

- Groceries (19% of Q4 2025’s online spending) maintained its position as the second-largest online category with 8% growth, driven by 7% higher transactions volumes while the average basket sized remained the same. This reflects the maturing of online grocery shopping as a routine part of busy Kiwi lives, rather than just a pandemic-driven necessity. Consumers have increasingly enjoying the convenience of a consistent basket compositions, providing grocery stores with a clear opportunity to drive growth through increased frequency.

- Department & General Merchandise stores (13% of Q4 2025's online spending): The stark contrast between online spending growth (7%) and instore decline (-1%) in this category reveals a fundamental shift in how Kiwis approach general merchandise shopping. The instore experience is becoming less important and shoppers appear happier to browse virtually. The offshore dominance (11% growth vs 3% domestic) further suggests consumers are becoming increasingly comfortable bypassing traditional local retailers for international platforms offering broader selection and competitive pricing. This presents an existential challenge for traditional department stores, who must either improve their instore value proposition or risk becoming showrooms for purchases that ultimately happen elsewhere.

HELPFUL HINT FROM NZ POST

Identify your category moment: Different sectors are experiencing different growth phases. Analyse whether your category is in growth, maturity, or transformation phase, and adjust your strategy accordingly. High-growth and transforming categories offer expansion opportunities, while mature categories require focus on differentiation and customer retention.

Regional performance: Growth everywhere but not equally

Q4 2025 saw online spending growth in every region, with the distribution revealing changing patterns in New Zealand's digital shopping evolution.

Fastest regional growth:

- West Coast: 15% spending growth; 14% transaction growth

- Southland: 14% spending growth; 15% transaction growth

- Waikato: 14% spending growth; 16% transaction growth

Slower regional growth:

- Marlborough: 6% spending growth (slowest); -5% average basket size

- Wellington: 7% spending growth; 9% transaction growth (joint slowest)

- Nelson: 10% spending growth; 9% transaction growth (joint slowest)

Auckland's performance deserves special attention, given it makes up around a third of the country’s total online spending. The region's 16% transaction growth was among the highest nationally but the 4% drop in basket size was also one of the biggest declines. This suggests Auckland consumers are shopping online more frequently but with smaller basket sizes, a pattern consistent with the urban trend toward convenience-driven, frequent purchases.

The strong performance in regions like West Coast and Southland indicates that online shopping adoption continues to spread beyond major urban centres, creating more opportunities for retailers to serve previously underserved markets.

HELPFUL HINT FROM NZ POST

Plan for the long game: With online's share continuing to grow, and shoppers transacting with higher frequency, ensure your digital infrastructure can handle increased transaction volumes. Focus on creating seamless and transparent checkout and delivery experiences that convert browsers into shoppers, and shoppers into fans.Find out how using a trusted delivery partner can help you drive growth.

What Q4 2025’s trend mean for retailers

Q4 2025's results paint a picture of a retail sector that's not just recovering but transforming. The 12% online growth rate significantly outpaced the 2% instore growth, continuing the structural shift toward digital channels. With online's share of total retail spending accelerating, we're witnessing not just Peak season success but fundamental market evolution.

The transaction-driven growth model - more purchases, smaller baskets - suggests consumers have become comfortable with online shopping as a regular activity rather than a special occasion. This behavioural shift creates opportunities for retailers who can optimise for frequency rather than just spending size.

The international versus domestic dynamic will continue to intensify. With offshore retailers growing transactions at more than double the rate of domestic retailers (24% vs 10%), New Zealand businesses need to leverage their local advantages to deliver speed, convenience, quality, value and a community connection.

PEAK 2025, DELIVERED BY NZ POST

Kiwi shoppers trusted us to deliver Christmas for them and we delivered, reaching 2.8m homes and businesses across Peak. We moved millions of festive parcels, including 40 tonnes of cherries and 70,000 food parcels. Customers embraced tracking their deliveries, leading to 3m app sessions and 27m website page views.

About our new data methodology

We're continuing to review and evolve our data methodology to ensure we deliver the most complete picture of New Zealand's online shopping landscape. This edition features a new approach using a variety of credible sources, moving beyond our previous reliance solely on card transaction data.

As online purchasing has evolved, we've expanded our data collection to include payments made through mobile apps, digital wallets, and other payment platforms that better reflect how shoppers transact today. To maintain accuracy in our comparisons, this new methodology has been applied retrospectively to previous reporting periods, ensuring all information is presented on a like-for-like basis.

We've also extended our analysis to provide more detailed sector category data, delivering more granular insights for retailers. As the eCommerce environment continues to evolve, we remain committed to refining our approach to capture the full spectrum of online shopping activity and deliver the most valuable insights for New Zealand retailers.