2025 was the year online shopping evolved from being the convenient alternative to becoming an integral part of how Kiwi shoppers buy every day. With online spending surging 10% on 2024, we saw fundamental channel, demographic and behavioural shifts in the retail landscape. Kiwi retailers were the big winners of these changes.

Online spending reached over $12.7bn in 2025, an increase of nearly $1.1bn from 2024, driven by both transaction (+6%) and basket size (+4%) growth. By comparison, instore spending was up by just 2%, driven by a small rise in transaction numbers.

Nearly one-in-four (23%) dollars of physical retail spend in 2025 was online, further cementing digital commerce as an essential part of New Zealand's retail landscape.

Key 2025 growth trends:

• Transaction frequency and increased basket size both drove growth, with shoppers making higher value purchases online, and with greater frequency.

• Domestic retailers outpaced international competitors, with more than double the rate of spend growth, driven by a significantly larger average transaction spend

• Online spending grew across all sectors, ranging from 6% to 34%, driven by transaction growth in all categories.

• Growth occurred right around the country, with smaller centres growing at a faster rate than the big cities.

• While the under 45’s still dominate online spending, the over 45's are growing quickly.

The numbers behind the growth

Annual online transactions grew by over 6 million transactions (+6%) while the average basket sizes increased to $120 (+4%).

2025 vs 2024 Snapshot

Online spending + 10% | Online transactions + 6% | Online average basket size + 4% |

This combination of more frequent transactions and higher basket values suggests a maturing market where consumers are feeling more confident to buy across more categories, and to spend more when they do. Online shopping is becoming woven into daily life rather than reserved for special purchases. We see this in the growth of everyday items like groceries and beauty products. At the same time, the increase in average basket size points to growing confidence in online channels for higher-value items. This is reflected in the growth in home and lifestyle sectors.

This balanced growth supports a healthy business model for retailers, with more frequent shopping driving cashflow and larger basket sizes improving profit margins and customer lifetime value.

HELPFUL HINT FROM NZ POST

Embrace the frequency opportunity: With online shopping becoming more every day, optimise your business for regular purchases rather than infrequent large orders. Consider subscription models, automated reordering, and loyalty programs that encourage and reward shopper’s frequent engagement.

International vs domestic

The domestic versus international battle also saw an important shift, tipping in favour of local retailers. Domestic retailers enjoyed nearly 80% of all online spending in 2025, with their share of online spending increasing at over double the rate of international spend.

While transaction growth was similar for international and domestic (6%), there was a big difference in basket size. New Zealand retailers strengthened their position with 5% growth in the average domestic basket sizes, while the average international basket shrunk by 1%. The average local basket is now a massive $53 greater than the international basket.

Domestic vs international 2025

Domestic share of 80% | Domestic spending + 11% | International spending + 5% |

Domestic & International + 6% | Domestic average $136+ 5% | International average $83- 1% |

It appears domestic retailers are competing effectively through their trusted local status and by differentiating on factors like quality, service, experience and convenience, rather than trying to take on global players on price.

HELPFUL HINT FROM NZ POST

Leverage your local advantage: New Zealand retailers are proving they can compete with international platforms. Focus on what makes you uniquely Kiwi - local relevance, faster delivery, easier returns, and genuine community connection. These advantages become more valuable as online shopping becomes routine, and the frequency of online scams rise.

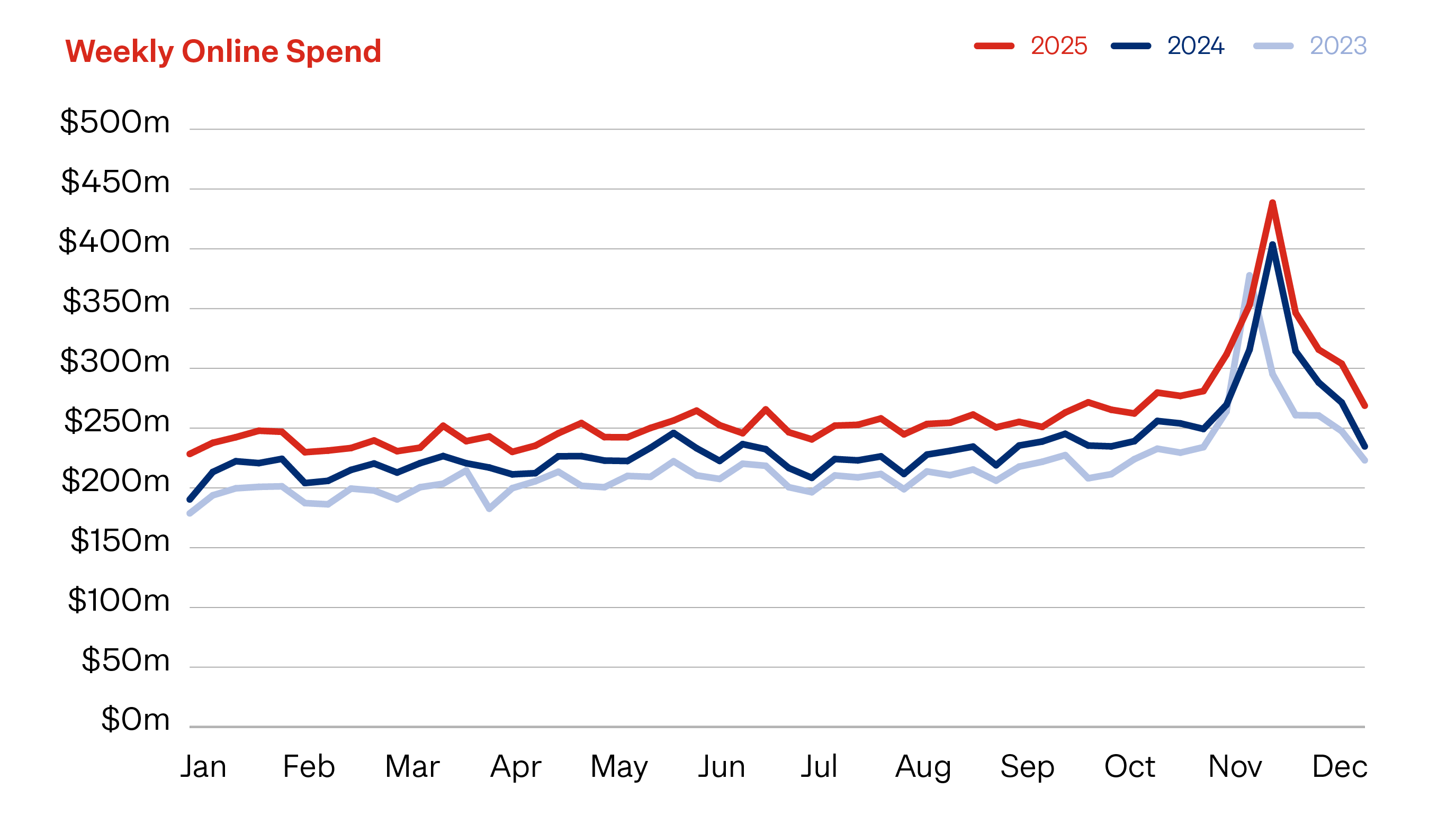

Q4 determines retailer’s success

Q4 (Oct-Dec) continues to be the most important part of a retailer’s calendar, with nearly 30% of the year’s online spending in the quarter. From Q3 2025 to Q4 2025 we saw a 22% lift in spending; a 19% lift in transaction volumes and a 3% lift in average basket size.

In recent years we’ve seen Kiwi shoppers spread their Christmas online purchases over a longer period. This extended sales period was also evident in 2025, resulting in strong growth for Q4 2025, up 11% on Q4 2024.

The peak of the quarter was the Black Friday to Cyber Monday extended weekend, with online spending 10% up on the same period in 2024.

Sector summaries

Online spending grew for all categories, although growth rates varied significantly. Domestic online spending outpaced international spending in all sectors. Homeware, Appliances & Electronics was the only sector to see a decline in international spending (-10%) while domestic spending for the sector grew by 9%. This may suggest that for larger value purchases, shoppers prefer to put their trust in local retailers.

Clothing & Footwear (17% online market share)

Spending growth (vs 2024) 8%(+8% domestic; +10% international) | Transaction growth (vs 2024) + 9% | Basket size movement (vs 2024) - 1% |

Department, Variety & Misc Retail (28% online market share)

Spending growth (vs 2024) 12%(+13% domestic; +9% international) | Transaction growth (vs 2024) + 2% | Basket size movement (vs 2024) + 5% |

Health & Beauty (2% online market share)

Spending growth (vs 2024) 35%(+39% domestic; +2% international) | Transaction growth (vs 2024) 42% | Basket size movement (vs 2024) - 5% |

Homeware, Appliances & Electronics (25% online market share)

Spending growth (vs 2024) 6%(9% domestic; -10% international) | Transaction growth (vs 2024) 1% | Basket size movement (vs 2024) + 5% |

Recreation, Entertainment, Books & Stationary (6% online market share)

Spending growth (vs 2024) 11%(15% domestic; +2% international) | Transaction growth (vs 2024) 10% | Basket size movement (vs 2024) + 1% |

Speciality, Food & Liquor (23% online market share)

Spending growth (vs 2024) 12%(+12% domestic; +6% international) | Transaction growth (vs 2024) 12% | Basket size movement (vs 2024) 0% |

Regional performance

2025 saw online spending grow across all regions. Strong performance in provincial cities suggests increased online shopping adoption in smaller centres.

Regional growth leaders:

• Southland and West Coast: Both achieved 15% spending growth, driven by both strong transaction and basket size growth.

• Bay of Plenty, Otago, Taranaki and the Waikato all had 12% growth in spending.

Regional growth under-performers:

• Marlborough and Wellington: Both recorded 6% spending growth, driven by 4% transaction growth and 2% basket size growth.

Auckland, which delivers around 31% of the national online spend, had solid growth (+9%). Christchurch had 12% growth in online spending. Wellington's lower comparative performance (+6%) may reflect the ongoing economic uncertainty in the capital.

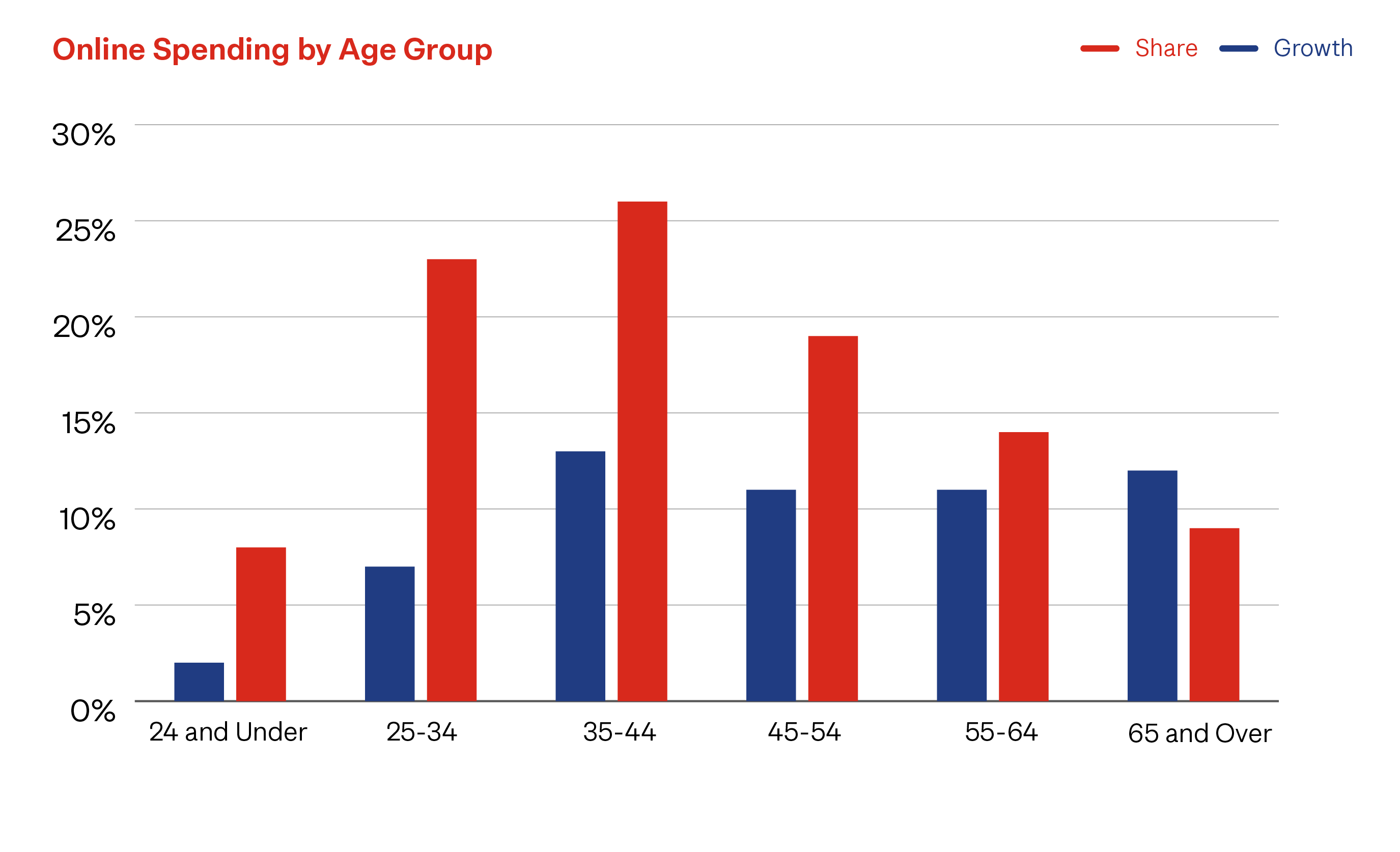

The generation shift

2025 revealed changing demographic patterns that are reshaping the traditional profile of online shopping. The 25-44 age brackets continue to dominate online shopping, making up nearly 50% of the spend in 2025. But we are seeing accelerated growth in both spend and transactions from the 45+ demographics, including the 65+ retiree market.

This demographic evolution suggests online shopping is crossing more generational boundaries as it becomes more familiar, routine and trusted. Older shoppers bring different expectations around service, quality, communication and support, creating new opportunities for retailers who can adapt their approach to serve these valuable customers.

HELPFUL HINT FROM NZ POST

Design for all generations: With older demographics experiencing online growth, ensure your digital experience works for customers who may prefer phone support, detailed product information, and traditional communication methods. Multi-generational design creates broader market opportunities.

Looking ahead: 2026 and beyond

2025 further cemented online shopping as an essential part of New Zealand life. Increases in both frequency and basket sizes, point to a more sustainable model that will benefit retailers as economic conditions improve over the year ahead. Despite ongoing market uncertainty, there are a number of key opportunities emerging for retailers:

1. Domestic market share gains suggest opportunities for local retailers to compete more effectively against international platforms but focusing on fulfilment and delivery experience, building trust and a local connection.

2. Routine shopping categories are likely to continue expanding online as consumers become comfortable purchasing everyday essentials digitally.

3. Demographic expansion into older age groups creates new customer segments with different needs and higher spending power.

4. Regional growth in smaller centres offers untapped market potential for retailers with regionally targeted digital strategies.

Given the turbulent start to 2026, it’s easy to think better times are some time away, but the reality is that we are already seeing week-on-week spending in Q1 2026 outstripping levels from a year ago. There’s never a better time for Kiwi online retailers to capitalise on the growth opportunities that changing shopper attitudes, behaviours and demographics bring.

Check out the latest Market Sentiments Report 2026 for more insights into how shoppers and retailers saw the last year, and their expectations for the year ahead. You can download it here.

About our new data methodology

We're continuing to review and evolve our data methodology to ensure we deliver the most complete picture of New Zealand's online shopping landscape. This edition of eSpotlight features a new approach using a variety of credible sources, moving beyond our previous reliance solely on card transaction data. Data was compiled and provided by leading data analysis firm, Dot Loves Data.

As online shopping has evolved, we've expanded our data collection to include payments made through mobile apps, digital wallets, and other payment platforms that better reflect how Kiwi shoppers purchase today. To maintain accuracy in our comparisons, this new methodology has been applied retrospectively to previous periods, ensuring all information is presented on a like-for-like basis.

We've also extended our analysis to provide more detailed sector category data, delivering more granular insights for retailers. As the eCommerce environment continues to evolve, we remain committed to refining our approach to capture the full spectrum of online shopping activity and deliver the most valuable insights for New Zealand retailers.

This article is for general information purposes only. From the actual data gathered, we’ve applied our experience and education in the industry to present these ideas and recommendations to consider. The views and opinions expressed, and any advice provided, is general in nature only. NZ Post does not represent that any information or advice it contains is suitable for your circumstances or purposes.